Cost of renewables to double by 2030

Still no serious alternative to the cost of Net Zero on offer

Introduction

In Autumn last year the Government released information on international energy prices. The data showed that in 2024 the UK had the highest industrial electricity prices in the developed world and the second highest domestic electricity prices. Before the election, Labour famously promised to cut energy bills by £300. However, it is now clear that energy bills are going much higher. When giving evidence to a recent Energy Security and Net Zero Select Committee hearing, Rachel Fletcher of Octopus Energy said that electricity bills would be 20% higher in four or five years’ time even if wholesale prices, largely set by gas, halve. Chris Norbury, chief executive of E.On UK had a similar message when he said even if wholesale prices go to zero, bills would be where they are today because of the increase in non-commodity costs.

The Department for Energy Security and Net Zero (DESNZ) continues to insist that:

“the only way to bring down energy bills for good is by making Britain a clean energy superpower, which will get the UK off the rollercoaster of fossil fuel prices and onto clean, homegrown power that we control.”

The briefing notes to the Kings Speech committed the Government to “speed up the build-out of vital grid infrastructure” which will add to the non-commodity costs the energy bosses were worried about in their testimony to ESNZ. The Government has also implicitly acknowledged that bills are going up, and the £300 commitment is dead because the Kings Speech notes also said “government estimates suggest that consumers could see a gradual accumulation of savings from 2030 onwards from Reformed National Pricing, reaching £20-40 on the typical annual dual fuel household bill by 2040.” In other words, bills are going to go up before 2030 and might possibly decline slightly afterwards.

In response to extremely high UK electricity prices, opposition parties have put forward some ideas to bring bills down. These initiatives have focused on cancelling AR7 contracts (Reform), eliminating carbon taxes and abolishing the Renewable Obligation Scheme early (Conservatives).

How much might current plans cost us, and would the opposition plans be enough to reverse that?

Renewables, Green Gas and Nuclear Subsidies

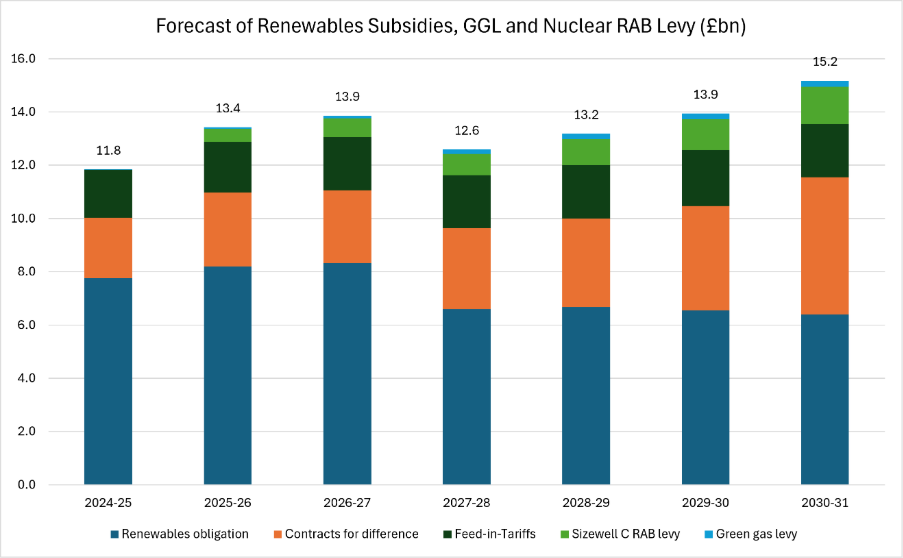

We can split the extra costs of energy into two categories. First, there are direct energy subsidies and second additional grid integration overheads that are largely driven by intermittent renewables. Helpfully, the OBR provides a forecast of the cost of environmental levies that includes subsidies from the Renewables Obligation (ROCs), Contracts for Difference (CfDs), the Green Gas Levy (GGL) and the Sizewell C RAB levy. The GGL subsidises green gas like biomethane and is levied on gas supply so also has a knock-on effect on electricity bills. The Government provided a forecast for Feed-in-Tariffs in a recent consultation. The total forecast for energy subsidies is shown in Figure 1 (all figures in nominal terms).

The total cost of these schemes is set to rise from £11.8bn in 2024/25 to £15.2bn by 2030/31. Within that total, the ROC scheme is forecast to rise from £7.8bn in 2024/25 to £8.3bn in 2026/27 before falling back to £6.4bn 2030/31 as Drax moves to a CfD and the subsidies expire for some of the oldest projects. We should note that 75% of the cost of the ROC scheme for domestic users is now borne by taxpayers and not billpayers. However, the current government plans to put the cost back on bills in April 2029. Abolishing the scheme in 2029 would reduce the burden on both domestic and non-domestic electricity consumers.

The cost of CfDs is forecast to rise from £2.3bn in 2024/25 to £5.1bn 2030/31. FiTs remain relatively stable, rising marginally from £1.8bn to £2.1bn by 2029/30 before falling back to £2.0bn in 2030/31. The Sizewell C subsidy goes up steadily from zero in 2024/25 to £1.4bn in 2030/31 and the GGL goes up to £0.2bn by 2030/31.

Note this analysis does not include the mooted Wholesale CfDs (WCfDs) proposed by Ed Miliband to give guaranteed market revenues to ROC-funded generators.

Grid Integration Overhead Costs

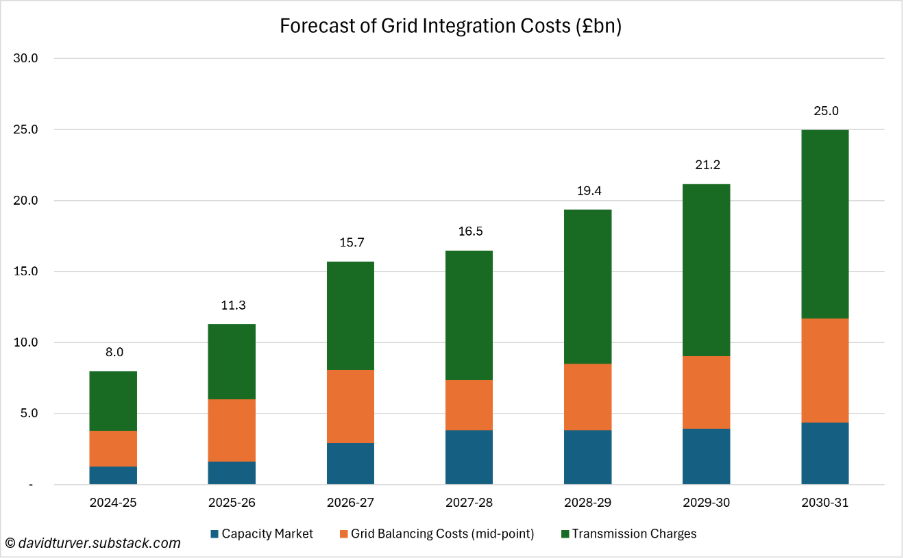

Grid integration costs include grid balancing costs, backup from the capacity market and the extra transmission costs incurred to connect remote renewables to the source of demand. NESO has provided a forecast of grid balancing costs and a forecast of transmission costs. The OBR forecasts the future costs of the Capacity Market. A summary of those forecasts is shown in Figure 2.

The total grid integration costs to accommodate the planned increase in renewables capacity to meet the current Clean Power 2030 plan are forecast to rise from about £8bn in 2024/25 to £25bn in 2030/31. Within that, Capacity Market costs are forecast to rise from £1.3bn to £4.4bn.

NESO provides several scenarios for grid balancing costs depending on whether they follow the Holistic Transition (highest balancing costs), Electric Engagement or Hydrogen Evolution (lowest balancing costs). For the purposes of this analysis the mid-point of the highest and lowest forecast in each year has been used. By this measure, balancing costs rise from £2.5bn in 2024/25 to £7.3bn in 2030/31. If plans to abolish carbon taxes and end ROCs early succeed (as suggested by some in the opposition), balancing costs may fall because some renewable generators will no longer be financially viable on a merchant basis. This potential impact has not been evaluated in this analysis.

NESO’s allowed revenues for Transmission Network Use of Service (TNUoS) costs rise from an actual cost of £4.2bn in 2024/25 to a forecast £13.3bn in 2030/31. It is interesting to note the forecast increase in TNUoS costs is larger than the increase in balancing costs the investment is supposed to mitigate.

Recent investor presentations from National Grid and SSE show they are salivating at the prospect of guaranteed returns from Ofgem to support spending to expand the grid.

Summary Total Cost of Subsidies and Grid Integration

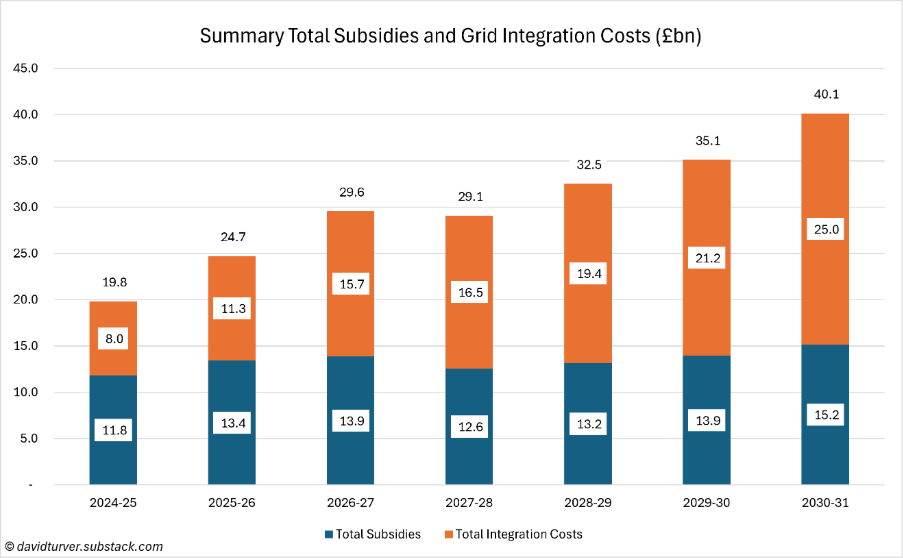

The total subsidies and grid integration overheads have been combined into a single chart in Figure 3.

Total subsidies and grid integration costs double from £19.8bn in 2024/25 to a staggering £40.1bn in 2030/31. These costs are likely to continue to increase as more renewables are built. Wind and solar curtailment costs will no longer be driven by grid capacity constraints, but by output being higher than demand. These staggering costs would be almost enough to buy a Hinkley Point C nuclear power plant every year.

As an aside, assuming the 77.3TWh of gas generation in 2025 was produced at 50% efficiency, the cost of the gas used for electricity at an elevated 100p/therm is about £5.3bn. It is clear the cost of gas for electricity is relatively trivial compared to the full costs of renewables.

Impact of opposition proposals

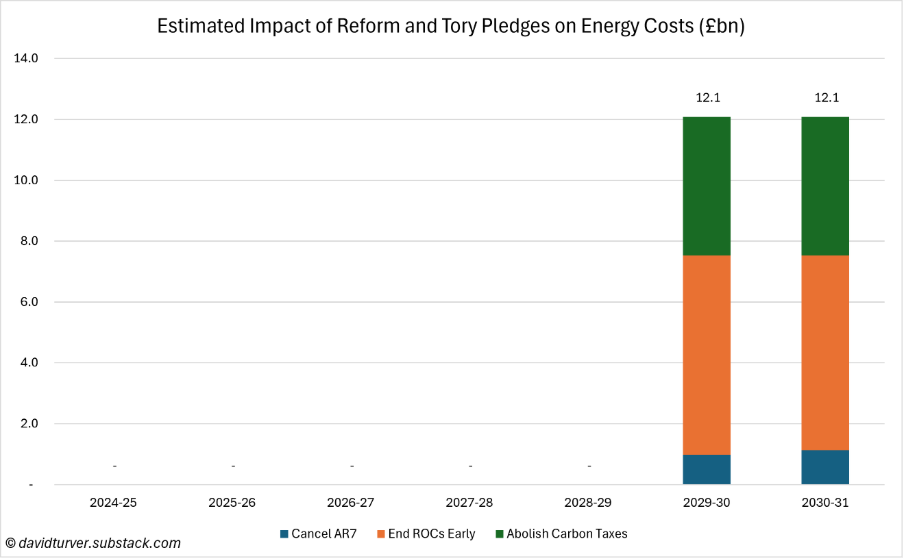

The forecast increase in subsidies and grid integration costs is obviously substantial. Some in the opposition have outlined plans to abandon net zero and bring energy prices down. Reform have pledged to cancel AR7 contracts and made vague promises to cut green levies. The Tories have been more specific, promising to end the ROC scheme early and to abolish carbon taxes on wholesale electricity.

To estimate the impact of these measures we need to make some assumptions. We will assume the aforementioned proposals become actual policy in time to have a full year effect in 2029/30.

The impact of cancelling the AR7 contracts has been estimated from the AR7 and AR7a results which give the budget impact by financial year (2024 prices). This gives a saving of £1bn in 2029/30 and £1.1bn in 2030/31. It should be noted that savings in later years will be larger as more offshore wind no longer comes on stream.

Estimating the impact of abolishing carbon taxes is a little trickier. Carbon taxes impact the wholesale price of electricity because wholesale prices are mostly set by gas. This means that these taxes not only impact the price of gas-fired electricity, they also impact the price of electricity from other generators too like nuclear, hydro, storage and ROC-funded renewables. From NESO’s generation mix and from Ofgem’s RER database, we can calculate that a total of 182.5TWh of electricity was generated by these sources in calendar year 2025 (excluding Drax ROCs that by 2029/30 will feature in CfD costs). Assuming carbon costs of approximately £25/MWh for 2025, per Ember, we can estimate the total carbon costs of electricity generation are about £4.6bn per year. Making a forecast of carbon costs in 2029/30 and 2030/31 is somewhat tricky, because by then there will be less gas and nuclear generation and ROC generation will be down too. Balanced against that, carbon costs may well have risen because of the government’s planned alignment with the EU Emissions Trading Scheme where carbon costs are higher. For the purposes of this analysis it has been assumed the carbon cost saving will remain £4.6bn in those years. It is also assumed that ending ROCs early will save the full amount in the OBR forecast. A summary of this analysis is shown in Figure 4.

The total impact of the opposition proposals could be around £12.1bn per year from 2029/30, if they were enacted in time.

It should be noted the Government has committed to remove the Carbon Price Support mechanism from April 2028 that should reduce carbon costs by around £1.5bn from April 2028. That is not included in this analysis. However, as will be shown below, it makes precious little difference to the big picture.

Impact of Changes

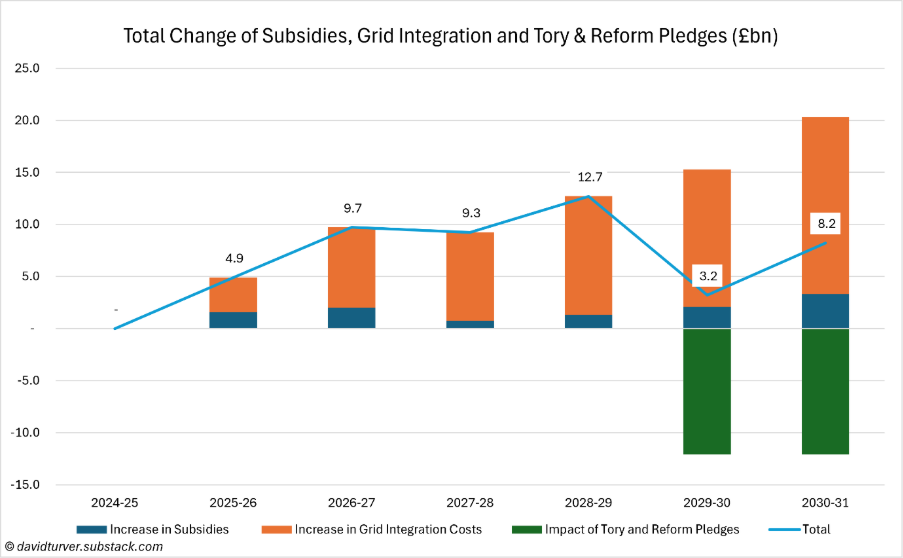

The full impact of the opposition proposals and the forecast changes in subsidies and grid integration costs from the 2024/25 baseline are summarised in Figure 5.

As we saw above, on the current trajectory, the increase in subsidies and grid integration costs from the 2024/25 baseline reaches over £20bn by 2030/31. This amounts to the equivalent of about £700 per household, without any change in gas prices. The opposition proposals would make a £12.1bn difference from 2029/30. However, the total impact of the forecast increases and proposals still means energy costs will be £3.2bn higher than 2024/25 in 2029/30 and £8.2bn higher in 2030/31.

Conclusions

In 2024 the UK had the most expensive industrial electricity prices in the developed world and second highest domestic prices. A national emergency to address this catastrophe should have been declared.

Instead, official forecasts shows that subsidies and grid integration costs are set to rise by over £20bn by 2030/31 from the 2024/25 baseline, further increasing electricity costs. This increase in costs amounts to the equivalent of £700 per household. The claims from Octopus and E.On that bills are going up regardless of what happens to gas prices can be seen to be true. It is clear that the often-heard claim that making Britain a “clean energy superpower” will bring down bills is false.

The pledges from parts of the opposition to begin to tackle high energy prices are very welcome, but not enough. Even if those pledges were fully implemented in time, electricity system costs will still be £8.2bn higher in 2030/31 than the baseline.

If the UK is to survive as a developed economy, these extra costs simply cannot be allowed to endure. In fact, drastic action will be required to cut subsidies even more than anyone in the opposition currently plans to do, and the extra grid integration overheads driven by intermittent renewables will need to be removed too. The legislative and contractual barriers to doing the right thing are considerable. It would mean inflicting considerable pain on the current beneficiaries of this state largesse – renewable energy generators, their investors, storage companies and grid operators. Investors in these doomed projects should take note.

However, the pain inflicted on the green blob by a return to a sane energy policy will be small compared to the pain inflicted on the rest of the economy if high electricity prices are allowed to continue. Net Zero must be stopped now.

| A guest post by

|

As a domestic energy user, events at the Strait of Hormuz mean that I am more driven by security of energy availability than by price - I also think that emerging technologies (eg Reflect Orbital - https://www.reflectorbital.com) will over the next 20/30 years transform energy as we currently know it.